How the 4% Retirement Rule Works

Understand the mechanics, history, and limitations of the famous 4% rule. Learn how to apply safe withdrawal rates to secure your early retirement strategy.

One of the foundational concepts in the FIRE (Financial Independence, Retire Early) movement is the 4% rule. It’s the formula used to calculate your FI number, your target retirement date, and—most importantly—how much you can safely withdraw from your portfolio once you cross the finish line. As the name suggests, the rule states you can withdraw up to 4% of your invested funds annually.

But there is a lot of nuance behind this simple heuristic.

For starters, it assumes your portfolio is a widely diversified mix of US stocks and bonds. The rule was originally popularized in 1994 by financial advisor William Bengen and later backed by the famous “Trinity Study.” By analyzing historical stock and bond data going back to 1926, researchers found that even through severe economic downturns, a 4% withdrawal rate historically never depleted a portfolio in less than 30 years.

However, what happens if your portfolio needs to survive longer than 30 years? The data is less definitive. Furthermore, the rule relies entirely on historical market performance, which is never a guaranteed roadmap for the 21st century.

Because of this, it’s best to treat the 4% rule as a rough guide rather than a strict law. In reality, withdrawals can be adjusted dynamically based on market conditions. During a down year, you can tighten your belt and withdraw less to preserve your capital. Conversely, during a massive bull market, you might withdraw a bit extra to pad a cash buffer account for future bad years.

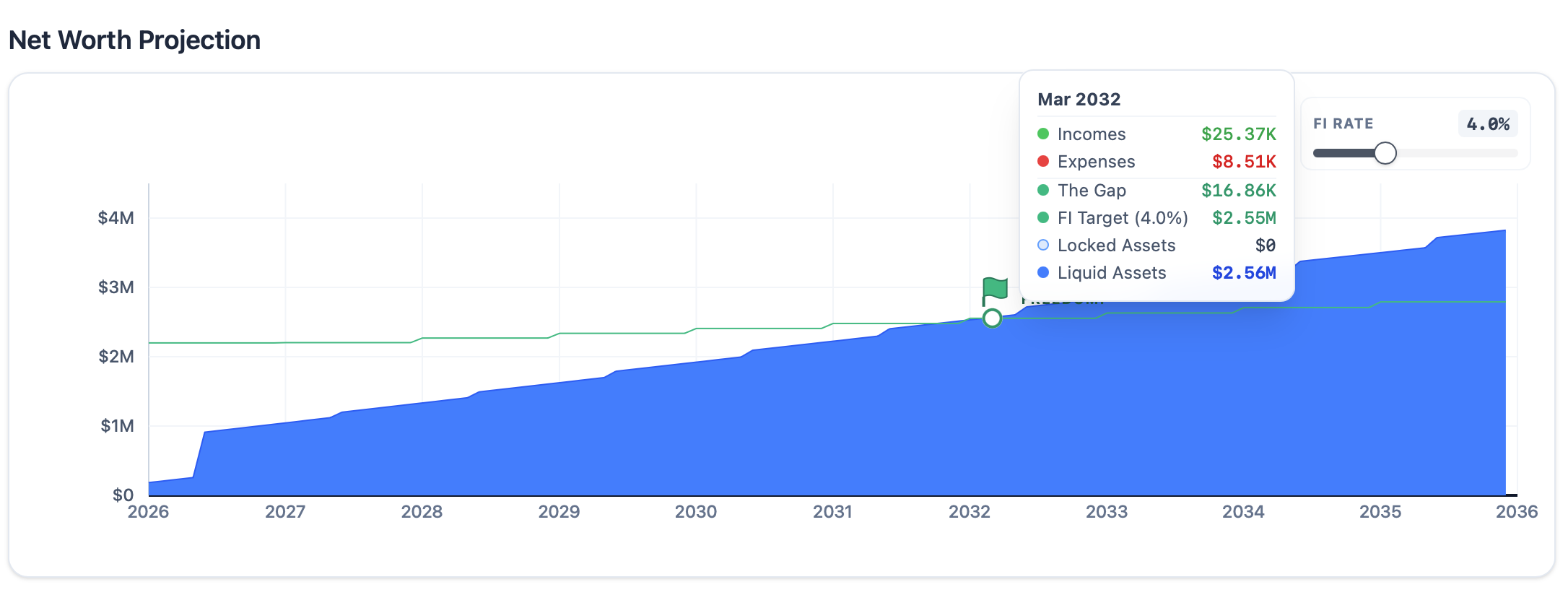

Using the 4% Rule to Find Your FI Date

At its core, Financial Independence means your investments generate enough to cover your living expenses. According to the 4% rule, if you can comfortably cover your yearly expenses by withdrawing 4% (or less) of your total investments—congratulations! You’ve achieved Financial Independence.

To figure out exactly what that target looks like, you take your current annual expenses and multiply them by 25 (since 100 / 4 = 25). That gives you your FI number—the total invested net worth you need to reach.

The second step is figuring out when you will actually hit that number. This is a bit trickier because it depends on several moving targets: your current invested balance, your monthly savings rate, and your estimated average annual return.

This is exactly where EasyFinancialPlanner does the heavy lifting for you:

The green dot shows that the networth projection will reach the FI number after 2032

Once you plug your assets, incomes, expenses, rules, and one-off events into the system, the projection engine automatically calculates your FI number and maps out your exact FI date.

It also gives you the flexibility to experiment. One of the best dials you can adjust in the app is your target FI rate. While 4% is the default, it doesn’t have to be your gospel. Bumping it up to 4.5% or 5% is a common strategy that can bring your Financial Independence date closer. On the flip side, dialing it down to a more conservative rate will push your date back, but offer a much wider safety margin for your retirement.