How a market downturn can affect your retirement

Understand Sequence of Returns Risk and discover strategies like cash buffers and bond tents to protect your retirement portfolio from market downturns.

When you are still working and building wealth, a market crash is often a good thing it’s essentially a giant sale on stocks that lets you buy more shares at a discount. But the moment you clock out for good and transition into retirement, that relationship flips completely. A downturn is no longer a buying opportunity; it becomes a direct threat to the survival of your portfolio.

Understanding how a market crash impacts your nest egg during this “decumulation” phase is critical to ensuring your money outlasts you.

The Danger of “Sequence of Returns Risk”

The single biggest threat a market downturn poses to retirees is Sequence of Returns Risk (SRR).

To picture how SRR works, imagine two retirees who end up with the exact same average annual return over a 20-year retirement, but they experience those returns in a completely different order:

Retiree A gets a strong bull market in their first five years, followed by a severe crash in year ten.

Retiree B retires directly into a major crash, suffering negative returns right out of the gate, followed by strong recovery years later on.

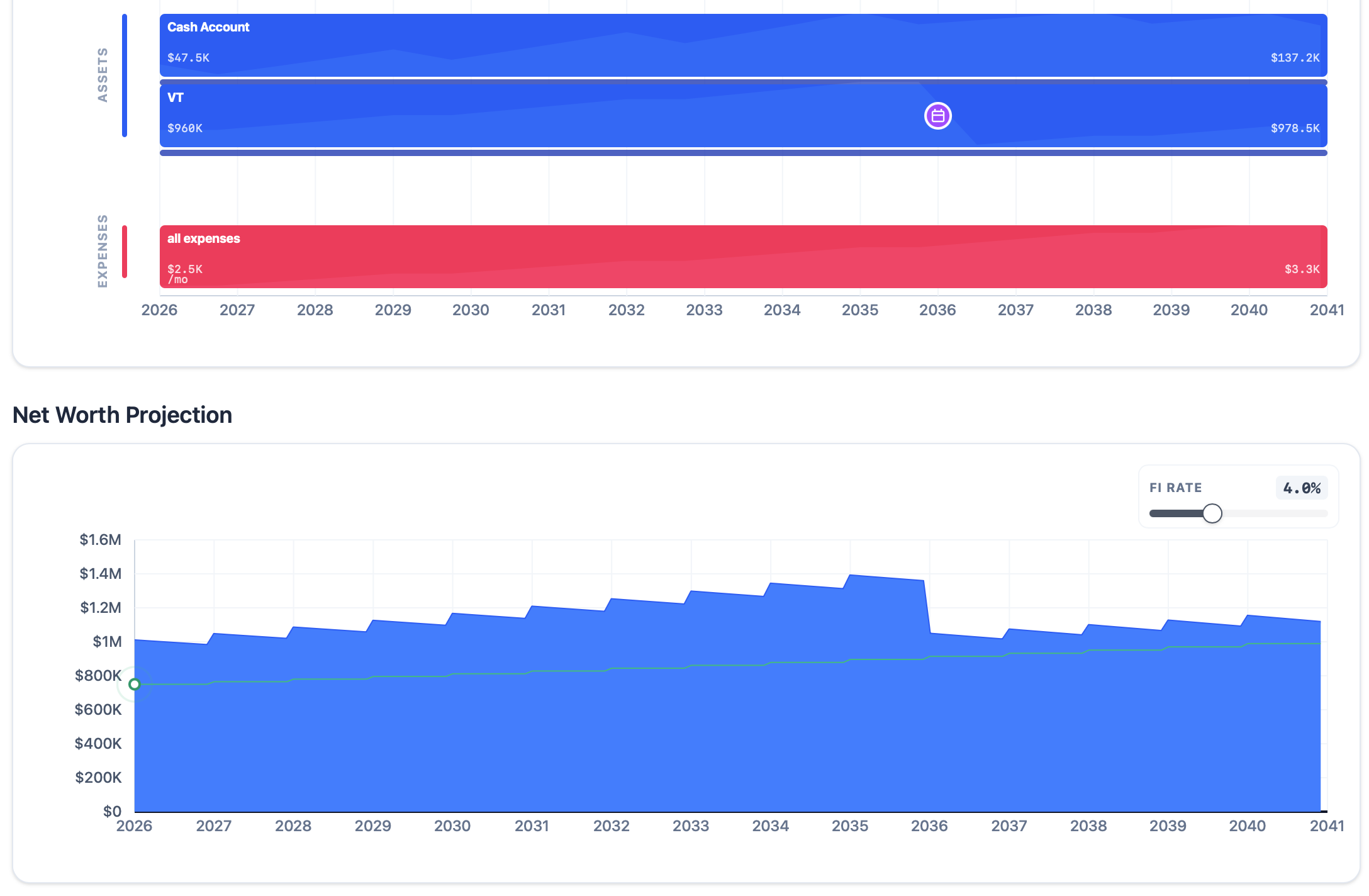

Retiree A: Late Market Crash (Crash in Year 10)

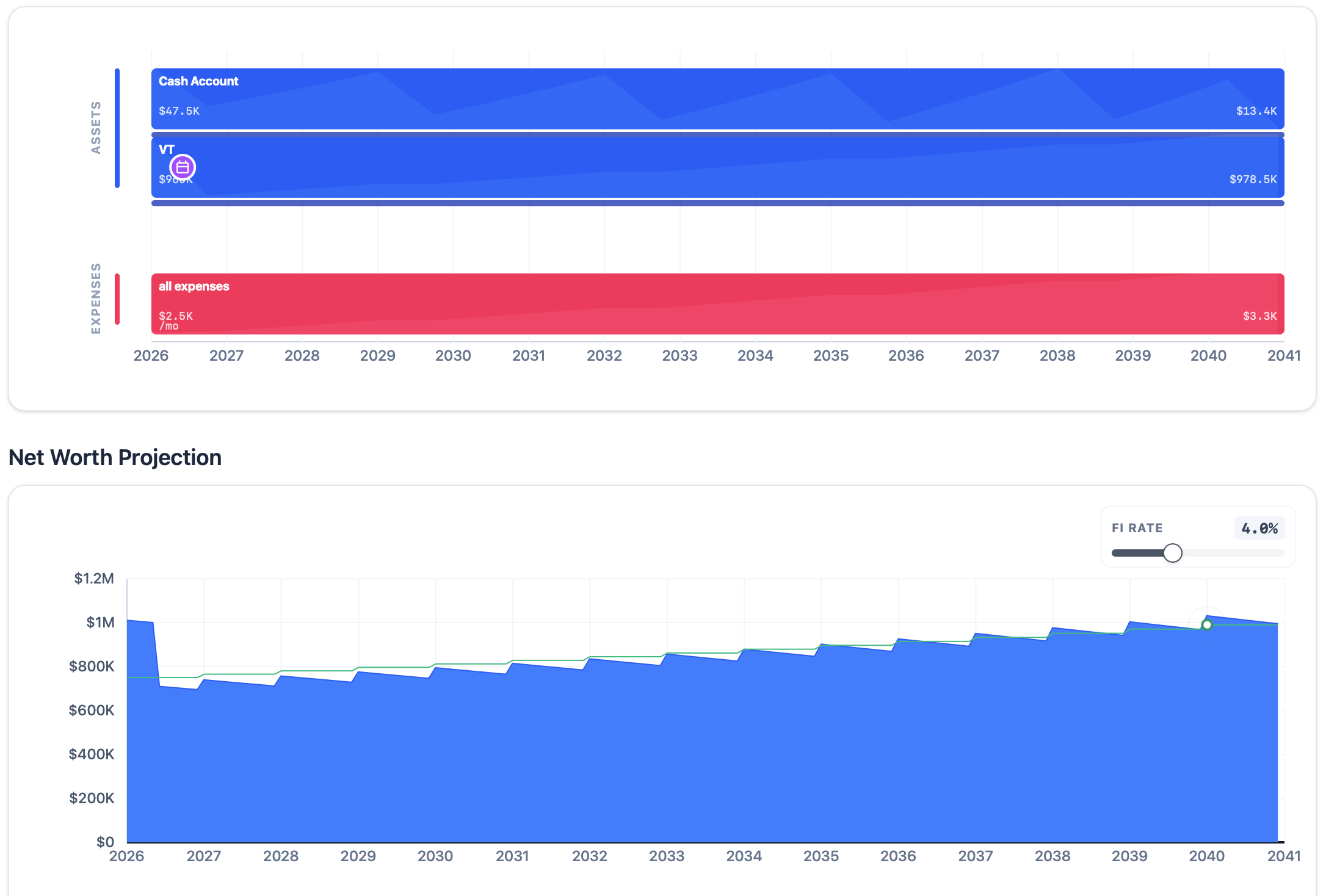

Retiree B: Early Market Crash (Crash in Year 1)

Even if their average return over those two decades is identical (say, 7% annualized), Retiree B at a higher risk of going broke.

Why? Because Retiree B still has bills to pay during that initial crash. By selling off assets at rock-bottom prices just to cover groceries and housing, they lock in those losses and permanently shrink their principal. When the market finally bounces back, Retiree B has a much smaller foundation left to capture those gains, making a full recovery incredibly difficult.

Notice that the investment account in both cases ends in the same amount but the cash account for retiree B is much smaller ($13.4k vs $137.2k). If spending was a bit higher, retiree B would have run out of cash and would have been forced to sell investments at the bottom.

Why the 4% Rule is Vulnerable

Many retirement plans rely heavily on the famous 4% Rule (withdrawing 4% of your portfolio every year).

While it is historically solid, the 4% rule assumes you are blindly following a static plan. If you happen to retire at the peak of a bull market right before a severe 30% or 40% drop, blindly pulling out that inflation-adjusted 4% will drain your accounts fast.

During a heavy downturn, that initial 4% withdrawal can easily morph into an actual withdrawal rate of 6% or 7% of your current, depleted portfolio value. That puts you straight into the danger zone.

How to Bulletproof Your Retirement

Luckily, you don’t have to just cross your fingers and hope the market behaves. Here are four proactive ways to protect your retirement from a crash:

1. Build a Cash Buffer (The “Yield Shield”)

One of the best ways to dodge Sequence of Returns Risk is simply not selling stocks when they are down. By keeping a cash buffer—usually 1 to 3 years’ worth of living expenses sitting safely in cash, high-yield savings accounts, or short-term bonds you can fund your life while giving your stock portfolio time to recover.

2. Stay Flexible with Spending

Instead of a rigid withdrawal amount, adopt a dynamic spending strategy. When the market takes a dive, tighten the belt on discretionary expenses like travel or big luxury purchases. Dropping your withdrawal rate by just 1% or 2% during the bad years can preserve a massive amount of your capital.

3. Use a “Bond Tent” or Guardrails

A bond tent is a strategy where you temporarily bulk up your safer assets (like bonds and cash) in the few years right before and right after your retirement date. Once you safely navigate that initial high-risk window (usually the first 5–10 years of retirement), you slowly transition back to your heavier, long-term stock allocation.

4. Stress-Test Your Scenarios

Don’t wait until a crash to see if your plan holds up. Use financial modeling to stress-test your numbers before you pull the plug on work. By mapping out a simulated 30% portfolio drop and seeing exactly how it impacts your long-term runway, you can tweak your retirement date or asset mix while you still have a steady paycheck.

This is easily done in EasyFinancialPlanner by using events. An event let’s you model market crashes and see how they impact your overall plan.

Market downturns are an unavoidable part of investing, but they don’t have to ruin your FIRE dreams. By understanding the risks and building a little flexibility into your roadmap, you can navigate the bumps with total confidence.