The Power of Compounding

Discover the mechanics of compound interest and see how small monthly contributions grow over time. Learn how to maximize your portfolio's compound growth.

Compounding is often called the eighth wonder of the world. Those who understand it, earn it; those who don’t, pay it.

In this post, we’ll look at a practical example of how a lump sum grows over time and how even small monthly contributions can significantly shift the final outcome.

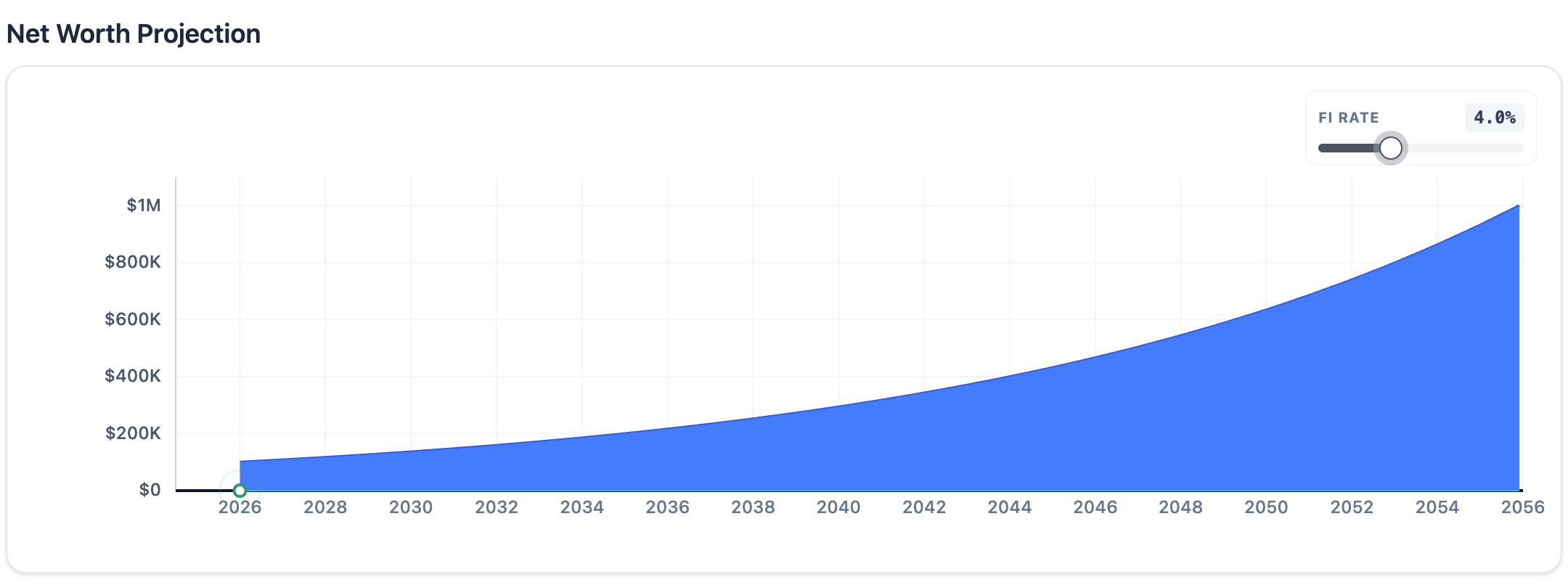

The Base Case: $100,000 Lump Sum

Let’s assume you have $100,000 in a cash account (or invested in a broad market index) with an average annual yield of 8%. If we compound this monthly, here is how that balance evolves over three decades:

- 10 Years: $221,964.02

- 20 Years: $492,680.28

- 30 Years: $1,093,572.97

Compounding growth of $100k lump sum

The most striking part is the jump between year 20 and year 30. In that final decade, the portfolio gains more than $600,000—more than it did in the first 20 years combined. This is the “hockey stick” effect of compounding.

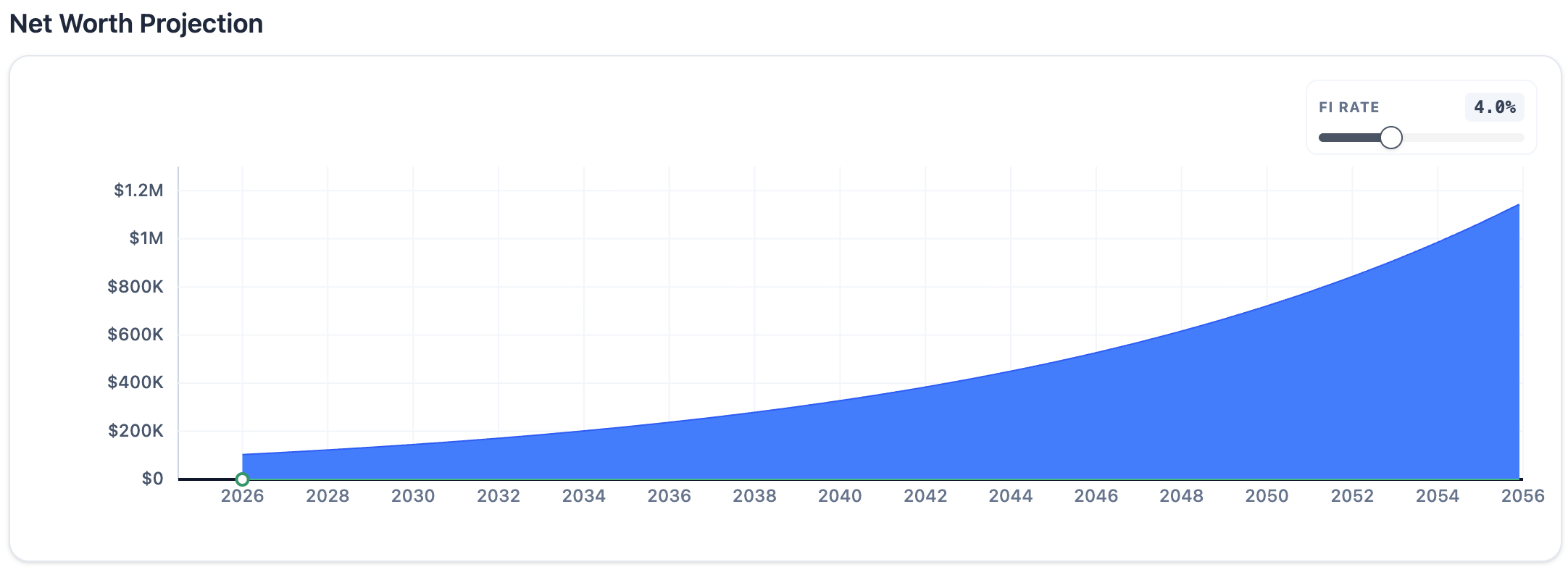

Adding Monthly Contributions

What happens if we add just $100 each month to this $100,000 start? It might seem like a small amount compared to the initial capital, but over long periods, the results are meaningful:

- 10 Years: $240,258.63 (+$18,294)

- 20 Years: $551,582.32 (+$58,902)

- 30 Years: $1,242,608.91 (+$149,035)

Compounding growth of $100k lump sum plus $100 monthly contributions

By contributing just $100/month (a total of $36,000 over 30 years), the final portfolio value increases by nearly $150,000.

Why This Matters

This simple analysis highlights two critical factors in financial planning:

- Time is your greatest asset. The real magic happens in the later years.

- Consistency adds up. Small, regular contributions leverage compounding to create results far beyond the literal sum of the deposits.

My goal with EasyFinancialPlanner is all about making these projections clear and easy to understand. Whether you are starting with $1,000 or $100,000, visualizing your trajectory is the first step toward financial independence.